1Q 2025 Recap & 2Q 2025 Outlook

Key Updates on the Economy & Markets

Stocks fell in the first quarter after two consecutive years of gains exceeding +20%. The year started off strong, with the S&P 500 reaching a new all-time high in mid-February. However, sentiment shifted late in February amid rising policy uncertainty in Washington, and the S&P 500 ended the quarter down. There are many moving pieces in markets today, and we want to take a moment to share our perspective. In this letter, we’ll recap the first quarter, discuss the drivers behind the recent market selloff, and provide an update on the economy.

Stocks Trade Lower as Valuations Moderate

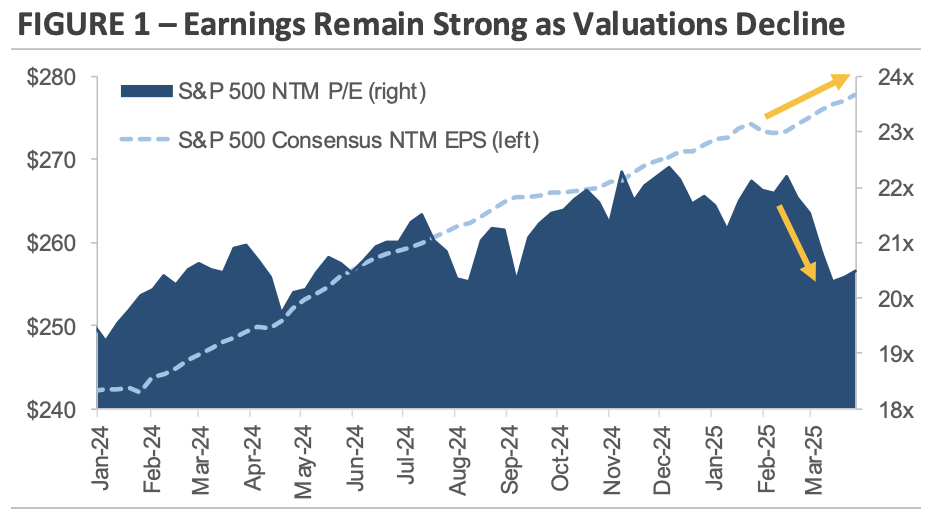

The big development in Q1 was falling stock market valuations, as rising policy uncertainty weighed on investor sentiment. Figure 1 provides context around the recent pullback, highlighting the divergence between earnings estimates and valuations. The dashed blue line graphs the rolling 12-month earnings forecast for the S&P 500, reflecting Wall Street analysts’ profit expectations for the year ahead. The navy shading graphs the S&P 500’s price-to-earnings (P/E) ratio, or how much investors are willing to pay for those future earnings. The chart shows earnings estimates tend to be less volatile than P/E ratios, which is natural as the market often swings between optimism and pessimism. The shift in sentiment during Q1, from optimism to caution, caused valuations to decline and stocks to fall.

Source: S&P Global. The price-to-earnings ratio (PE ratio) is a valuation metric used to assess how much investors are willing to pay for each dollar of a company’s earnings. EPS is based on NTIM consensus estimates. NTIM = Next 12-months. Latest available data as of 3/31/25.

The right side of the chart shows Wall Street analysts slightly lowered their earnings forecast in Q1, citing the potential for tariffs and slower growth. Meanwhile, the S&P 500’s P/E ratio declined from over 22x to around 20x. The valuation decline may seem modest, but it had a meaningful effect on returns. Those falling valuations were the primary driver of the selloff as sentiment weakened. Investors started to price stocks more conservatively due to concerns about tariffs, slower economic growth, and policy uncertainty.

Company size impacted returns during the quarter, as market leadership shifted and last year’s top performers lost momentum. Last year, the Magnificent 7, a group of leading tech stocks that includes Nvidia, Microsoft, Alphabet, Amazon, Tesla, Apple, and Meta, delivered an impressive +63% return. The group’s strength lifted the broader market, with the S&P 500 gaining +23%. In contrast, the equal-weight S&P 500, which gives all companies the same weight regardless of size, gained only +11%. This year, the dynamic has flipped. Instead of lifting the market, the biggest stocks are now dragging it down. The Magnificent 7 has declined -15% year-to-date, while the equal-weight S&P 500 is down only -1%. The takeaway: smaller companies held up better during the selloff.

Rising Policy Uncertainty is Impacting Sentiment

Developments in Washington took center stage in Q1 as the Trump administration started rolling out its policy agenda. The administration’s early efforts focused on trade policy, tariffs, and reducing government spending. The policies are a notable shift from the status quo and have drawn attention from investors and business leaders due to their potential impact on the economy.

The charts in Figure 2 graph three measures of sentiment. The datasets provide insight into how households, business leaders, and investors view current conditions and what they expect in the future. Tracking sentiment can help gauge potential shifts in consumer spending, business investment, and overall economic momentum.

The top chart graphs the University of Michigan’s Consumer Sentiment Index, which tracks how optimistic or pessimistic consumers feel about the economy. Consumer sentiment weakened early in the pandemic and hit a record low in June 2022. The decline reflected concerns about rising inflation, expectations for higher interest rates, and broader economic uncertainty. Sentiment gradually recovered from late 2022 through the end of 2024, as inflation eased, economic growth exceeded expectations, and stocks set record highs. However, sentiment has turned downward again in early 2025. The reversal signals renewed concern among consumers, who have been a key driver of economic growth in recent years.

Source: University of Michigan, The Conference Board, CBOE. Latest available data as of 3/31/2025.

The middle chart graphs The Conference Board’s CEO Confidence Index, which measures how optimistic business leaders are about conditions. Since the 2010s, the index has fluctuated between 5 and 8. Recent years were especially volatile due to pandemic disruptions, persistent inflation, high interest rates, and geopolitical and policy uncertainty. In Q1, the index fell to 5.0, the lowest level since October 2011. The decline signals increased caution among CEOs as they navigate changing policy, the potential for tariffs, and an uncertain economic environment.

The bottom chart graphs market volatility during the first quarter, as measured by the CBOE Volatility Index (VIX). Volatility increased in early 2025, starting in mid-February. Some market volatility is normal, but the recent spike occurred as policy uncertainty increased and the stock market sold off. Markets dislike uncertainty, and until there is more clarity, market volatility could remain elevated.

The three measures of sentiment signal a more cautious tone among consumers, business leaders, and investors. This matters because sentiment can impact future behavior. Consumers may cut back on spending, while businesses may delay hiring or investment decisions. Sentiment data will remain in focus in the coming months as more policy details are released.

An Update on the U.S. Economy

It is important to remember that the stock market isn’t the economy. In other words, the performance of the stock market doesn’t always reflect real-time economic conditions. This is because the market is forward-looking and prices in expectations for what’s to come. The previous section highlighted how rising policy uncertainty affected sentiment in Q1, and this section examines the latest economic data. Figure 3 on the next page graphs four economic indicators that offer insight into the state of the U.S. economy: the unemployment rate, retail sales, housing starts, and industrial production.

The top chart graphs the unemployment rate, which remains low by historical standards. Unemployment rose in 2023 and the first half of 2024 as workers reentered the labor market and job growth slowed. This led to concerns about labor market softening and contributed to the Federal Reserve’s decision to start cutting interest rates in September 2024. However, unemployment reversed lower in recent months as monthly job growth picked up. The data points to a resilient labor market, with demand for workers running up against a still relatively tight labor market.

The second chart graphs the year-over-year growth of retail sales, a measure of consumer spending. Growth was strong in 2023, supported by rising wages and the continued drawdown of pandemic-era savings. However, growth slowed in 2024, an indication that while households continue to spend, they’re doing so more cautiously. Potential factors include high interest rates, persistent inflation, and a return to more typical spending patterns. Consumer spending makes up almost 70% of U.S. GDP, so a continued slowdown could have implications for the broader economy.

The third chart graphs the year-over-year growth of housing starts, which are a leading indicator of housing activity. The housing market slowed in recent years as it struggled under the weight of high mortgage rates and decreasing affordability. Homebuilders were hesitant to take on new projects amid weaker demand and elevated borrowing costs, and recent policy announcements are creating more uncertainty. Tariffs and immigration policies create potential challenges for builders, as they may raise material costs and decrease labor availability. However, despite the headwinds, housing starts are still above pre-pandemic levels.

Source: Department of Labor, U.S. Census Bureau, and Federal Reserve. Latest available data 3/31/2025.

The fourth chart graphs the year-over-year growth of industrial production, which measures the total output of factories, mines, and utilities across the economy. Industrial activity was flat or declined in 2023 and 2024 as high interest rates and economic uncertainty dampened business investment. More recently, industrial output shows signs of recovery, with industrial production growing at the fastest pace since late 2022. The rebound likely reflects expectations for lower interest rates and the resolution of uncertainty after last year’s election. The question is how tariffs will impact manufacturing as 2025 progresses.

Together, the data suggests the U.S. economy is losing some momentum. However, they also show the economy continues to expand, just at a slower pace. The labor market remains solid, and consumer spending is holding steady. The housing sector has cooled from its pandemic highs, but it still exceeds the pace from the 2010s. Meanwhile, manufacturing activity is showing renewed strength. The risk moving forward is that policy uncertainty could weigh on confidence and trigger a slowdown. Economic data will be in focus in the coming months.

Equity Market Recap – Looking Beyond the Index

Most of the stock market decline occurred in the second half of the quarter, after the S&P 500 set a new all-time high on February 19th. As mentioned earlier, a small group of mega-cap stocks drove the selloff, and their size and weight within broad stock market indices impacted performance trends. The Growth factor, which holds many of these high-profile mega-cap stocks, returned -10% in Q1. Similarly, the Nasdaq 100, an index of leading technology companies that include the Magnificent 7, returned -8%.

Sector returns highlight the concentrated nature of the selloff. Nine of the eleven S&P 500 sectors outperformed the broad index to start the year. Seven of those sectors posted gains, while the other two were flat. This is a sharp contrast to last year, when a handful of sectors powered the S&P 500’s gains. Technology and Consumer Discretionary, two of last year’s top performers, are the two worst-performing sectors this year. It’s not a coincidence that these sectors are the most exposed to the Magnificent 7, which has weighed on their returns just like the broader S&P 500. In contrast, sectors that underperformed in 2024 are the top-performing sectors this year. While the S&P 500 is down by -4.3%, the average stock within the index is down -1%.

International stocks outperformed U.S. stocks in Q1, posting one of its biggest quarters of outperformance since 2000. The underperformance of U.S. mega-cap tech stocks contributed to international’s outperformance. Outside the U.S., the MSCI EAFE Index of developed market stocks gained +8% in Q1. Much of that strength came from Europe, where investor sentiment improved as governments unveiled plans to increase spending. This triggered a rotation out of U.S. stocks and into Europe in anticipation of increased government spending leading to stronger economic growth. Meanwhile, the MSCI Emerging Index gained +4.5% in Q1, underperforming the developed index but outperforming the S&P 500 by nearly +9%.

Credit Market Recap – Bonds Trade Higher in Q1

There were two notable themes in the bond market in Q1: falling U.S. Treasury bond yields and wider credit spreads. The 10-year Treasury yield fell from a peak of around 4.80% in mid-January to 4.15% in early March. It was a reversal from Q4, when the 10-year yield rose more than +0.75% due to renewed inflation concerns. Several factors contributed to the Q1 reversal, including rising policy uncertainty, the potential for tariffs, and concerns about slower economic growth. The combination prompted investors to move money into longer-maturity government bonds, which are viewed as safe havens. Bond prices rise as yields decline, and Treasury bonds provided diversification benefits in Q1, offsetting a portion of the stock market decline.

Another major theme was credit spread expansion. Credit spreads measure the difference in yield between high-yield corporate bonds and safer government bonds, such as U.S. Treasuries. Spread levels can serve as a real-time gauge of market sentiment, showing how easy or expensive it is for companies to borrow money. A narrower spread signals that investors view credit risk as low, while a wider spread signals higher perceived default risk.

Figure 4 graphs the high-yield credit spread since 1997. The high-yield spread narrowed in late 2024 as the Federal Reserve cut interest rates, reaching levels last seen in 2007. However, the yellow circle shows credit spreads widened in Q1. The increase indicates investors are becoming more cautious, with the potential for tariffs and slower economic growth leading to higher credit risk.

Despite the recent rise, the chart shows credit spreads remain low by historical standards. Compared to past periods of market stress, today’s spread levels suggest financial conditions are still relatively stable, a reflection of the U.S. economy’s overall strength. While investors are concerned about policy uncertainty and the potential for slower growth, the market is not signaling financial distress. However, if spreads continue to widen, it could signal tighter financial conditions and raise concerns about potential defaults. The market will be watching spreads closely.

Source: Federal Reserve (ICE BofA US High Yield Option-Adjusted Spread). Latest available data as of 3/31/2025.

2025 Outlook – Maintaining a Long-Term View

Market volatility can be unsettling, but it’s a normal part of investing. Periods of enthusiasm often lead to recalibration. It’s natural to feel uncertain, but history shows that staying invested through volatility and maintaining a longer-term perspective is the prudent approach.

Figure 5 puts the Q1 market volatility and selloff into perspective. It uses almost a century of S&P 500 price data to show that market pullbacks like this year are not just common—they're a healthy and recurring part of investing. The chart graphs annual drawdowns, or the largest peak-to-trough decline within each calendar year. The bars show the S&P 500 experiences a pullback nearly every year, with a median intra-year drawdown of -13%. Since 1928, the S&P 500 has experienced a drawdown of -5% or more in 91 out of 98 calendar years, including 2025.

Source: S&P Global. Index performance is for illustrative purposes onlyand does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results. Latest available data as of 3/31/2025.

The chart highlights a fundamental reality of investing: market corrections are a normal part of the cycle. These periods can be uncomfortable, but they serve the important functions of resetting valuations and curbing speculative excess. Without occasional declines, markets could become dangerously overextended, increasing the risk of more severe and extended downturns.

Despite these frequent and sometimes severe drawdowns, the S&P 500 has delivered strong returns over nearly a century. This is despite wars, recessions, inflation spikes, financial crises, and a global pandemic. The upward trajectory is driven by economic growth, innovation, and corporate earnings growth. The key takeaway for investors: volatility isn’t a sign that something is broken—it’s the price of admission to investing. Staying invested through ups and downs has consistently been one of the most effective strategies for building wealth over time. Market declines can feel unsettling in the moment, but history shows the powerful effect of compounding returns over time.